Break a home down payment goal into monthly targets, timelines, and realistic trade-offs. This guide explains down payment savings plan in a practical way: what to calculate first, which assumptions matter, how to compare scenarios, and which related tools can help you avoid a misleading headline number.

Key takeaways

- Start down payment savings plan planning with one baseline number, then test a conservative and optimistic scenario.

- Use the same time period, units, and assumptions when comparing options.

- Calculator results are estimates; verify high-stakes financial, tax, legal, or medical decisions with qualified professionals.

- Strong decisions combine the number, the formula, the example, and the next step.

Why down payment savings plan matters

Break a home down payment goal into monthly targets, timelines, and realistic trade-offs. The goal is not to memorize a formula. The goal is to make the inputs visible, compare choices consistently, and avoid decisions based only on a headline number. For many everyday money decisions, down payment savings plan is useful because small changes in rate, time, payment size, or unit conversion can create a large difference over months or years.

A good down payment savings plan process starts with context. A calculator can answer the immediate question, but the explanation tells you whether the answer is stable, sensitive, or only a rough estimate. That is why each DollarCalcGuide guide pairs calculators with formulas, examples, FAQs, and related links rather than publishing a number by itself.

Searchers usually arrive with a narrow question: a payment amount, a percentage, a conversion, a payoff date, a savings target, or a revenue estimate. The best page answers that narrow question quickly, then expands into the decision behind it. This structure improves usefulness for readers and gives search engines clearer signals about the intent of the page.

A practical method

Start with the smallest useful version of the problem. Define the amount, the rate or percentage, the time period, and the unit. Then calculate one baseline scenario and two alternatives. This keeps down payment savings plan simple enough to use while still showing the trade-offs that matter.

For money-lite topics, the most important habit is consistency. If one option is monthly and another is annual, convert both to the same period. If one result uses nominal dollars and another uses inflation-adjusted dollars, label them clearly. If a page involves units, convert before comparing. These steps reduce false confidence.

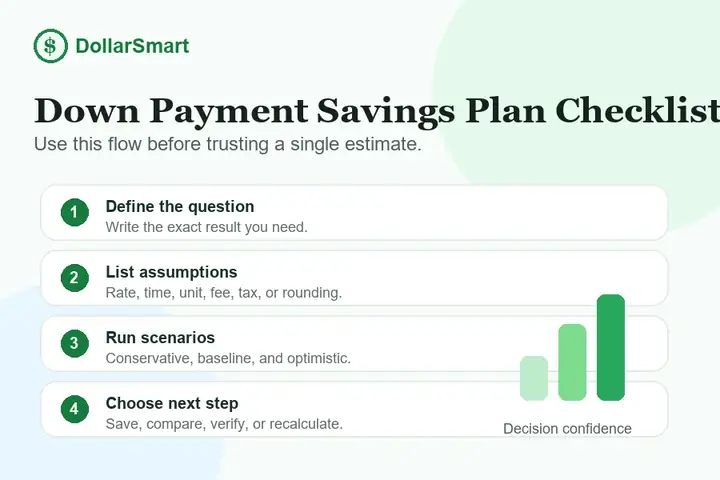

- Define the question. Write the exact number you want to answer before using a calculator.

- List assumptions. Note rates, time periods, tax assumptions, fees, units, and rounding choices.

- Run a baseline. Use the values that feel most realistic today.

- Stress test the result. Change one input at a time so you can see what drives the answer.

- Choose a next step. Save more, compare offers, verify a rate, or open a related calculator.

Worked example

Imagine two options appear almost equal. After entering the numbers, the calculator may show that one option has a lower monthly cost but a higher long-term total. That difference is exactly why formula-based pages are useful: they turn hidden trade-offs into visible numbers.

For example, a lower payment can come from a longer term rather than a better price. A higher savings projection can come from an aggressive return assumption rather than a larger contribution. A larger percentage change can look dramatic even when the original amount is small. In each case, down payment savings plan becomes clearer when the input values are visible.

A practical example should include the starting value, the formula, and a short explanation of the result. Do not round too early. Do not compare unlike units. Do not ignore one-time fees just because the recurring number looks comfortable. If the decision affects a budget, create a cash-flow version of the calculation as well as a total-cost version.

Scenario comparison

| Scenario | What to change | What to watch |

|---|---|---|

| Conservative | Use a weaker rate, higher cost, or slower timeline. | Can the plan still work if conditions are less favorable? |

| Baseline | Use the most realistic current estimate. | Does the result fit your budget, time, or target? |

| Optimistic | Use a better rate, lower cost, or faster timeline. | Is the upside meaningful enough to justify the risk? |

Scenario comparison is especially important for down payment savings plan because the first result is rarely the only useful result. A range helps you understand sensitivity. If a small input change creates a large output change, the decision deserves more review before you rely on it.

Common mistakes

The most common mistake is treating an estimate as a guarantee. Another is ignoring small recurring costs because they look harmless in isolation. A third is comparing annual, monthly, weekly, daily, or unit-based numbers without converting them to the same basis.

Another mistake is using a calculator only once. Better decisions usually come from changing one variable at a time. If down payment savings plan depends on a rate, change the rate. If it depends on time, change the time horizon. If it depends on a starting value, test a smaller and larger amount.

Finally, avoid copying a result into a decision without reading the assumptions. A calculator is strongest when it makes the assumptions obvious. If you cannot explain why the output changed, the result is not ready to guide an important action.

Related tools

Use these related calculators and reference pages to turn down payment savings plan into a clearer plan. Internal links are grouped by intent so you can move from a guide to a calculator, a conversion, or a nearby article without starting over.

Frequently asked questions

What is the safest way to use down payment savings plan?

The page explains the assumptions, formula, examples, and related tools so you can understand the number rather than just copy it.

How often should I update my down payment savings plan numbers?

The page explains the assumptions, formula, examples, and related tools so you can understand the number rather than just copy it.

Which calculator helps with down payment savings plan?

The page explains the assumptions, formula, examples, and related tools so you can understand the number rather than just copy it.

Can down payment savings plan estimates replace professional advice?

The page explains the assumptions, formula, examples, and related tools so you can understand the number rather than just copy it.

Why should I compare more than one scenario?

The page explains the assumptions, formula, examples, and related tools so you can understand the number rather than just copy it.